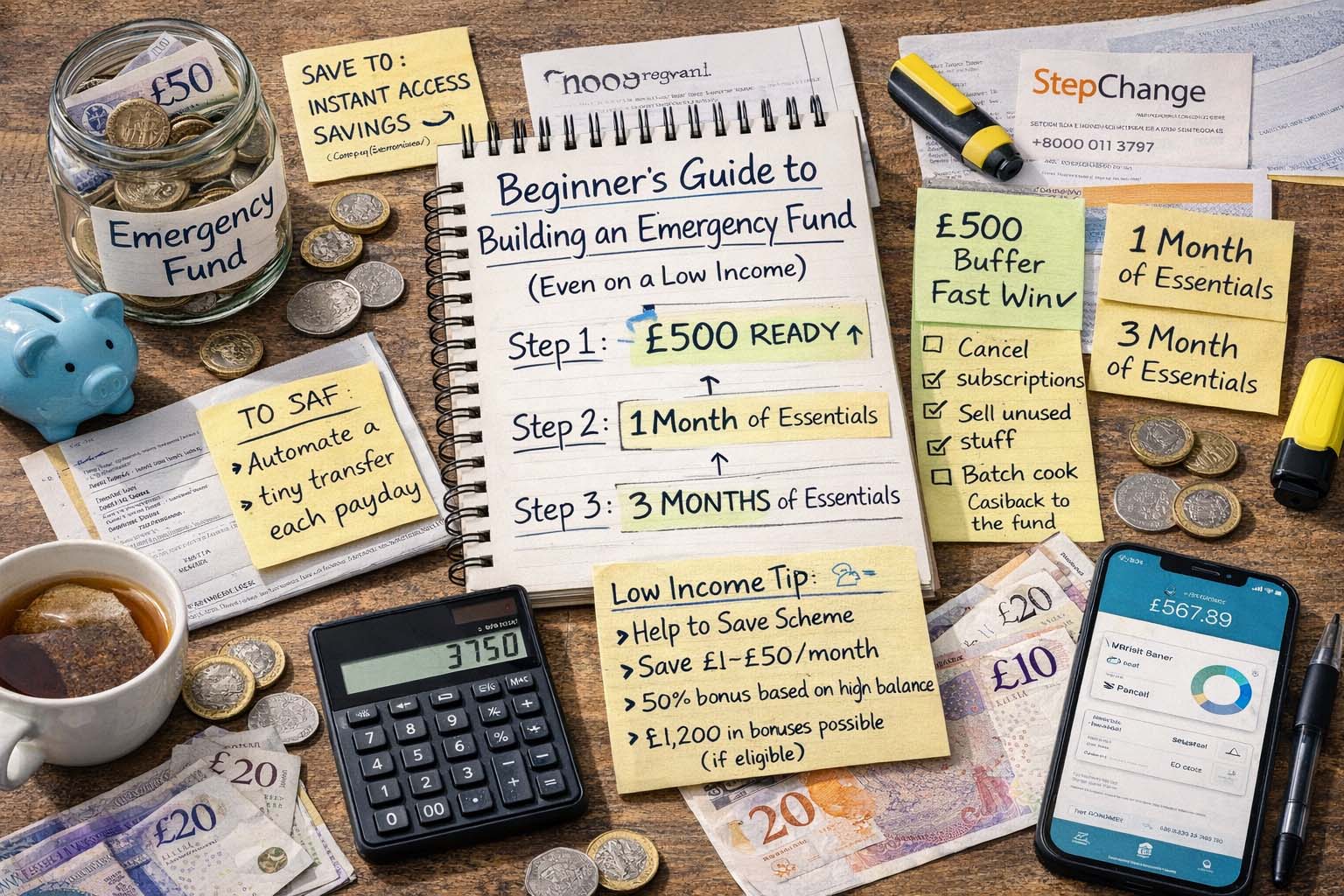

Step-by-step: £500 → 1 month → 3 months

An emergency fund is cash you can access quickly when life happens: a broken boiler, urgent travel, a car repair, or a sudden drop in income. It’s not glamorous — but it’s one of the strongest “stress reducers” you can build.

In the UK, a common rule of thumb is 3–6 months of essential outgoings in an instant access savings account.

If that feels impossible right now, don’t start at “3 months”. Start in levels.

Before You Start: A 2-Minute Check (Debt + Safety)

If you have high-cost debt (credit cards, payday loans, unauthorised overdraft) or arrears (rent/mortgage, Council Tax), MoneyHelper advises it’s usually cheaper long-term to prioritise those before putting all spare money into savings.

Practical approach for most people:

- Build a tiny buffer (even £50–£200) so one surprise doesn’t push you into more debt.

- Then focus on the expensive debt.

- Then scale your emergency fund.

(If you’re struggling, StepChange offers free debt advice and budgeting support.)

Step 1: The Starter Fund — £500

Why £500?

Because it covers many “real life” emergencies without needing credit: a repair call-out, a replacement phone, a train ticket home, a childcare gap.

How to reach £500 on a low income (choose 1 plan)

Plan A: £10/week → ~50 weeks

Plan B: £20/week → ~25 weeks

Plan C: £2/day → ~250 days

Even £5–£10 a week helps build resilience, especially when money is tight.

Your “£500 Fast Wins” list

Pick 2–3 and redirect the savings automatically:

- Cancel/ pause unused subscriptions (even 1–2 helps)

- Switch a couple of branded items to own-brand weekly

- Batch cook 2 dinners/week (reduce takeaways)

- Sell 5 unused items (Facebook Marketplace/Vinted)

- Put all cashback/reward money straight into the fund

Step 2: One Month of Essentials — 1 Month

Now you’re moving from “small shocks” to “life disruption”.

Calculate your Essential Monthly Outgoings (not total spending)

Include:

- Rent/mortgage

- Council Tax

- Gas/electric/water

- Basic food

- Travel to work

- Minimum debt payments

- Childcare essentials

- Insurance you genuinely need

Example: Essentials = £1,250/month

✅ 1-month fund target = £1,250

MoneyHelper frames emergency savings as a cushion based on essential outgoings, not lifestyle spending.

Step 3: Three Months of Essentials — 3 Months

This is the milestone where people often feel the biggest stress drop.

Target = Essential monthly outgoings × 3

Example: Essentials £1,250/month

✅ 3-month target = £3,750

MoneyHelper’s guidance commonly references 3–6 months of essential outgoings as a solid cushion.

If your income is irregular (self-employed, gig work, commission), lean closer to 6 months once you can.

Where to Keep Your Emergency Fund (So It Actually Works)

Your emergency fund should be:

- Instant/easy access (not locked away)

- Separate from spending money (to reduce temptation)

- Used only for “true emergencies”

Safety: choose a UK-authorised provider (deposit protection)

UK deposits are protected by FSCS up to £120,000 per eligible person, per authorised firm (from 1 Dec 2025).

The System That Makes Saving Possible: “Pay Yourself First”

The biggest secret is not motivation — it’s automation:

- Open a separate savings pot/account

- Set an automatic transfer for payday (even £5–£25)

- Increase it when something gets cheaper (bill drops, debt cleared)

If you remove the decision each month, you save more consistently.

Low-Income Booster: Help to Save (UK)

If you’re eligible, the government’s Help to Save scheme can supercharge small savings:

- Save £1–£50/month

- Earn a 50% bonus based on your highest balance at 2 years and again at 4 years (up to £1,200 total bonus)

- It’s government-backed via NS&I, and you can withdraw money (but read the scheme rules first).

This can be a powerful way to build an emergency fund if you’re on a low income and qualify.

What Counts as an “Emergency” (Use This Rule)

Yes:

- Boiler/washing machine breakdown

- Essential car repair for work

- Emergency travel

- Unexpected medical/dental cost (if applicable)

- Job loss / reduced hours

No (plan for these separately):

- Holidays

- Christmas

- Birthdays

- Routine car servicing

- “Good deals” sales

A simple rule: If it’s urgent, essential, and unexpected — it’s an emergency.

How to Use Your Fund Without Killing Your Progress

When you withdraw money:

- Pay for the emergency

- Pause extra goals (extra debt overpayments, investing) for 1–2 months

- Rebuild back to the last level (e.g., from £900 back to £1,250)

This keeps one emergency from turning into a financial spiral.

Common Problems (and Fixes)

“I keep dipping into it.”

Make it harder to touch:

- Keep it in a separate bank/app

- Remove the card (if offered)

- Rename it: “Do Not Touch Fund”

StepChange recommends keeping emergency savings separate and using it only for genuine emergencies.

“I can’t save anything.”

Start with “micro-savings”:

- £1–£3 on good weeks

- Round-ups

- One no-spend day/week

Then scale when a bill changes or a debt is cleared.

“Should I save or pay off debt?”

As general guidance, if debt is expensive (credit cards/unauthorised overdraft), it often makes sense to prioritise clearing it — while keeping at least a small buffer so you don’t fall back into borrowing.

Quick Emergency Fund Plan (Copy/Paste)

Week 1: Open separate instant access savings + set £5–£25 auto transfer

Weeks 2–8: Build to £100–£200 buffer

Next: Push to £500

Then: Build to 1 month of essentials

Then: Build to 3 months of essentials

FAQ

How long will it take?

It depends on the amount you can save monthly — but the goal is momentum. Even small, steady savings are meaningful over time.

Should I keep cash at home?

A small amount can be useful, but most emergency funds are safest in an account you can access quickly (and ideally protected).

What if my partner and I share expenses?

You can build a joint fund, or each keep your own. What matters is that the household can handle an emergency.

If money is tight, don’t aim for perfection. Aim for levels:

£500 → 1 month → 3 months.

Every step reduces stress and reliance on debt.

This article is general information, not personalised financial advice. If you’re dealing with arrears or debt pressure, consider free UK support such as MoneyHelper and StepChange.

-

-

-

-